IDEX Online Research: The Jewelry Pipeline's Coming Compression & Consolidation

June 06, 06

Editor's Note: The following is a synopsis of

Consolidation and compression of the jewelry and diamond pipeline - the channel of distribution from mine to market - will drive new efficiencies over the next two-to-three years, yielding greater profits for pipeline participants. However, that same consolidation and compression will eliminate a large number of marginal competitors, especially those who add little value, leaving primarily those participants who are both highly vertically integrated and add significant value to the product when it passes through their hands.

Jewelry Pipeline: Who Is Winning . . . And Who Is Not

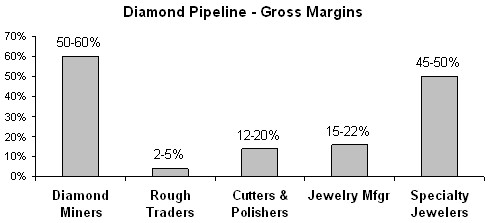

The current jewelry pipeline is too fragmented to operate efficiently. This fragmentation also results in lack of pricing power with nearly every link in the distribution chain.

While both ends of the pipeline - miners and retailers - generate solid earnings, those participants in the middle barely eke out a living due to depressed profit levels. In the words of

Longer term, as a result of lack of profitability and earning power, many of the pipeline participants, especially those in the middle, will disappear as their functions are absorbed by highly vertically integrated competitors who add value at several levels of the jewelry pipeline.

Mining Drives the Jewelry Pipeline

The 'upstream' end of the jewelry pipeline where raw materials - diamonds, gold, gemstones, silver, etc. - are mined is highly profitable. In part, these returns are necessary to support the level of capital investment necessary to fund a mining operation, including exploration and other soft costs. In part, lack of competition due to very high barriers of entry allows these companies to post such large profits. For example, over $2 billion was invested in the Diavik mine in

Gemstone and Precious Metals Traders Add Little Value

The next link in the jewelry distribution chain - the traders of gemstones and precious metals - earn the lowest margin of any participant in the jewelry pipeline. That¡¦s no surprise, since they add virtually no value, other than to redistribute the raw materials used in the manufacturing process of jewelry. If the DTC can't get it right - that is, the Sight boxes don¡¦t have the right mix of stones - the stone traders make the corrections. Arguably, these traders help match supply and demand. However, when viewed from afar, they are not a necessary part of the jewelry pipeline. If the miners took a more active role in distribution of raw materials based on market demand (and perhaps cutters¡¦ and polishers' expertise), they could possibly eliminate most of the rough diamond traders.

Recently, two key participants in the rough diamond trading business confirmed that this is nearly a no-margin business.

- Tiffany, in a recent conference call with Wall Street analysts, explained that its corporate gross margins were depressed due to increased sales of unusable rough diamonds. Management said its wholesale diamond business - the sale of rough stones that are not high enough quality for Tiffany jewelry - was a low-to-no margin business.

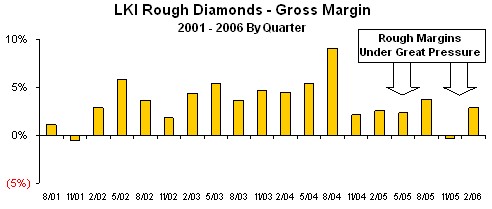

- Maurice Tempelsman, chairman of the board of Lazare Kaplan explained recently that rough diamond trading margins are opportunistic. Rough diamonds, he said, are a commodity with low margins. They trade at a high velocity, and traders don't want to hold inventory, he continued. "We want to sell exactly what we buy," he said. Tempelsman said that he expects rough diamond trading margins to remain in the 2-3 percent range for the foreseeable future. The graph below summarizes recent rough diamond trading margins for Lazare Kaplan. As shown on the graph, during the quarter ended November 2005, the company lost money trading rough diamonds.

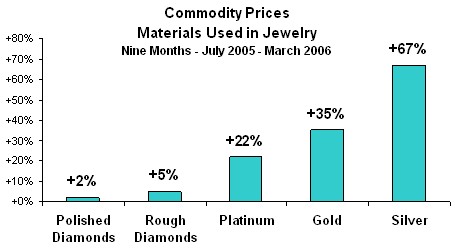

Lazare Kaplan does not speculate in diamonds because there is no way to lay off risks. With most commodities, the financial markets have developed tools to hedge price risks. However, the diamond market has no financial instruments to attenuate risk. Some would argue that this is good news. While most commodities have soared in price recently due largely to financial speculators, neither rough nor polished diamond prices have risen notably, as the graph below illustrates.

Source: Commodities markets & IDEX Online

In addition to modest margins and the lack of risk attenuation tools, diamantaires are under more pressure than ever to avoid holding inventory. With the elimination of De Beers' buffer stock, rough diamond prices have been more volatile, a trend that will likely continue. So far, interestingly, volatility of rough diamond prices has not been reflected in polished diamond prices. Nor has volatility in precious metals prices been reflected measurably in retail prices of gold and silver jewelry, though platinum jewelry (less than 2 percent of the retail market) has experienced some upward price pressure.

There is one reasonable scenario under which traders might remain in the pipeline: if they embraced the Wall Street trading model, including its total transparency and the possibility of a futures market. This model does not work well except when large firms with very high trading volumes dominate the business.

Cutters & Polishers: No Pricing Power

While those in the next link of the jewelry pipeline - the cutters and polishers of gemstones and precious metal jewelry - add significant value, their margins are also very modest. In part, this is because of high industry fragmentation. No single producer is large enough to have any pricing power. This is still a 'mom-and-pop' business.

The most likely outcome for cutters and polishers is absorption by pipeline links on either side of them. As pipeline leaders look for ways to remove costs, cutting and polishing functions can be readily absorbed into a vertically integrated infrastructure, with operational profits accruing to the owners of the vertically integrated businesses.

High Volume Is the Key to Profit

Jewelry manufacturers, the next link in the distribution chain, also generate modest gross margins - generally in the 15-20 percent range. Again, because of fragmentation in the jewelry manufacturing sector, no one has pricing power. Thus, only the larger, more efficient producers will survive longer term.

Jewelry Retailers: Adding Emotional Value

Jewelry retailers, after miners, are perhaps the most important link in the jewelry pipeline. They are responsible for adding tremendous intangible value to each piece of jewelry. For example, they must convince consumers that diamonds, which are literally no more than unusual pieces of gravel, are worth a lot of money based on scarcity and emotional value (think 'A diamond is forever', 'Past, Present, and Future', and other tag lines that tug at the heart strings). They are responsible for taking silver, at $12-14 per ounce, and selling it to customers for many times that value based solely on an emotional appeal (silver can't be sold on scarcity, because it is not scarce).

The best evidence of the value that is added by specialty retail jewelers can be observed by comparing margins between online jewelry merchants and store-based jewelers. Store-based jewelers' margins approach 50 percent; they add value through plush environments, superior selling skills, and tactile inventory. Online merchants, on the other hand, don't offer these value-added amenities, and their margins are much lower.

Retail Jewelers: Margins Under Siege

Despite sharply rising prices of many of the commodities used in jewelry manufacturing, savvy jewelers never try to sell jewelry based on potential "financial investment" value. Jewelry may be an emotional investment, but it is not suitable as a financial investment.

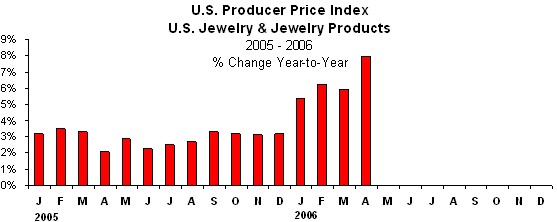

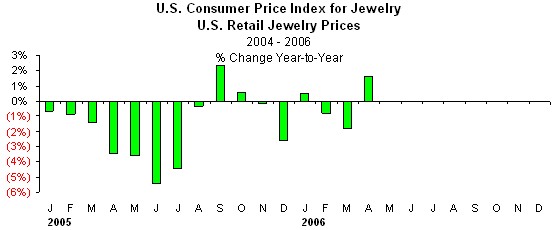

Retail jewelers' margins are declining, primarily due to the failure to raise retail prices in the face of increased costs. Because of fragmentation among retail jewelers - the top four have 24 percent of total market share compared with other retail categories where the top four have 50-70 percent market share - no single jewelry has pricing power. Recent data (see graphs below) from the U.S. Department of Commerce shows that the jewelry Producer Price Index (PPI) is soaring upward while the jewelry Consumer Price Index (CPI) remains flat. Jewelers can expect increased margin pressure in 2006, unless they raise retail prices.

Jewelry Producers' Prices Are Up . . .

Source: BLS

. . . But

Source: BLS |

Evidence of Jewelry Pipeline Consolidation Abounds

Compression and consolidation of the jewelry pipeline is well underway.

- Aber has "book-ended" the jewelry pipeline. It owns a diamond mine, and it owns Harry Winston luxury jewelers. Aber chairman Bob Gannicott has followed both the money and the margins that exist at both ends of the jewelry pipeline, but that are scarce in the middle of the distribution chain.

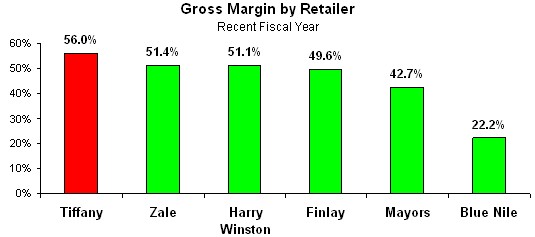

- Tiffany now has a DTC Sight with a partner. In addition, it sells rough diamonds, and it has jewelry manufacturing operations. Tiffany is probably the most highly vertically integrated jeweler in the industry, and it generates the highest margins of any of its primary competition, as the graph below illustrates.

Source: Company reports |

- Signet Group recently said that it was looking into vertical integration in the jewelry pipeline, especially related to rough diamonds. Signet¡¦s management cited several benefits of sourcing its own rough diamonds, including the following: 1) security of supply; 2) consistency of quality and price; 3) better understanding of supply into the polished diamond market; and 4) possible reduction of costs. Some in the industry believe that Signet would like a DTC Sight. However, from a financial viewpoint, this would be a questionable strategic move.

- Zale continues to increase its direct sourcing initiatives by integrating more deeply into the jewelry pipeline. Zale's moves are eliminating wholesalers and other suppliers who do not add value.

- Movado, the watch manufacturer, operates 55 Movado stores - which generated about $85 million of sales in 2005 - making it the 17th largest specialty jeweler in

- Wal-Mart is, of course, the king of consolidation and compression of its distribution pipeline. Producers have a direct pipeline into Wal-Mart stores, unhampered by wholesalers, jobbers, suppliers, and any others who add little or no value. This could eventually become the model for all retail categories, including the jewelry industry.

Specialty Jewelers: A Vanishing Breed?

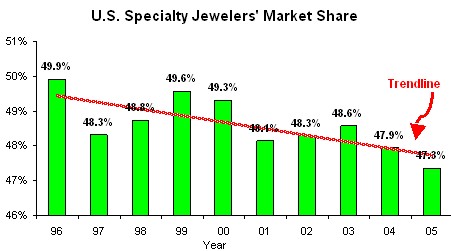

While specialty jewelers add value to the jewelry pipeline, there is major consolidation in this sector. For the past several years, the total number of specialty jewelers in the

However, more worrisome to the specialty jewelry industry, the market share of specialty jewelers in

Source: Dept. of Commerce

Specialty jewelers are losing market share to discounters, mass market retailers, and other specialty retailers such as apparel and accessory merchants. In addition, online jewelry retailers have taken market share from specialty retailers.

The most vulnerable independent specialty jewelers are those who try to compete head-to-head with Kay, Zale, Helzberg, and other mass market jewelers. Those who are likely to survive will carve a niche at either the high-end of the market or at the lower-end where popular-priced jewelry is sold largely on credit.

Further, if independent specialty jewelers are to survive competition from both chain jewelers and non-traditional outlets from jewelry, there are going to need to re-invent their business. Suggestions for independent jewelers include the following:

- Review your competitive differential every day.

- Partner with reliable vendors who will listen to you.

- Forget ego: move your store, downsize, increase sales productivity.

- Add sales people. There is a high correlation between the number of sales people in a jewelry store and aggregate store sales.

- Raise your average ticket.

- Listen to your accountant.