IDEX Online Research: Online Retailing vs. Store Retailing: Two Different Businesses

February 25, 10

Online jewelry retailing is an entirely different business from store-based jewelry retailing. Unfortunately, many jewelers do not understand this concept. They simply try to take the merchandise in their store and put it on line. It’s not that simple, and it usually results in failure.

The economic business model for online retailing – and specifically online jewelry retailing – is vastly dissimilar traditional store-based business models as well as other non-store retailing models such as catalog merchants, television shopping, and others.

Online retailing requires a new mindset – merchants must be able to look at retailing in a new, out-of-the-box way. For example, the online retailing business model operates with gross margins so low that the resulting gross profit dollars would not cover the operating expenses of the traditional store-based jeweler. Retailers who think they can sell jewelry online for the same prices that they charge in their stores will find quickly that their customers have become ex-customers.

Further, most online retailers don’t own their inventory; in contrast, store-based retailers own their inventory for about a year before they sell it. Online retailers need little working capital; store-based jewelers are heavy users of working capital and short term debt.

Beyond the differences in the financial model, the business model for selling online is also different. Rather than romancing a beautiful diamond eye-to-eye with a customer standing only eighteen inches away, an online retailer must create the same mystique with a customer who might be a world away. There is no way online sales people can read a customer’s body language. In short, the sales process is entirely different.

In the past, jewelers were slow to embrace the internet. Today, most jewelers have a website, but most do not engage in online commerce.

Online jewelry sales represent about 4 percent of total industry sales, based on 2008 data (the latest available); industry sales were about $60 billion in 2008. About three-fourths of online jewelry sales are comprised of diamonds and diamond jewelry. Because diamonds have been reduced to a commodity, it is very easy to sell them online. In contrast, other types of jewelry have not been commoditized, so selling those goods online is much more difficult.

Online Sales for Chain Jewelers Modest

So far, online retailing has not been an important source of revenue for chain jewelers. For example, Zale generated about $56 million of online sales for its fiscal year ended July 2009, or just over 3 percent of sales.

Online Jewelry Business Model Difficult to Forge

There have been many attempts to sell jewelry online, but most have failed. Names that litter the retail road to failure include Odimo, BodyFlash, Adornis, EnJewel, ValueAmerica, Miadora, and others (we note that some of these names are still registered, but generally redirect viewers to other jewelry and non-jewelry sites).

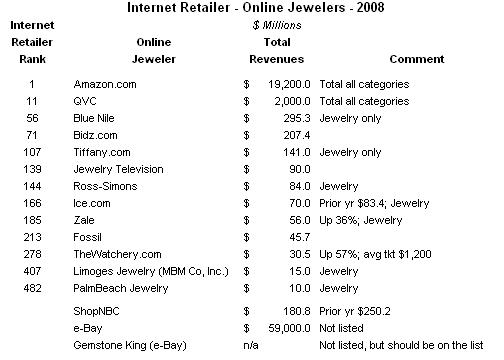

Who’s Selling Jewelry Online?

The magazine Internet Retailer conducts an annual census of online retailers by product category. While they don’t break out individual sales by merchandise line, they do provide aggregate sales levels by company.

The following table summarizes online jewelry merchants rankings for 2008, the latest data available. Interestingly, e-Bay was not listed on the Internet Retailer rankings for jewelry, despite it being a major retail jewelry distributor. We listed e-Bay at the bottom of the table, along with another couple of omissions.

Source: Internet Retailer |

There is only one viable public jewelry company which generates all of its revenues from online commerce:

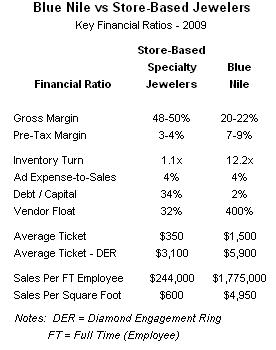

The following table compares key financial measures of Blue Nile versus the typical specialty jewelry in

Source: Blue Nile, Jewelers of America & Other |

Here are comments about the key financial ratios shown on the table above:

· Gross Margin – Online jewelry retailers like

· Pre-Tax Margin – Because online jewelers have a much lower operating cost structure – no store rent, no ambiance – their operating costs are much lower than store-based merchants. Thus, online retailers are able to generate a much larger pre-tax profit – roughly double the level of a store-based jeweler.

· Inventory Turn – There is a dramatic difference in the inventory turn of an online merchant like

Many jewelers believe that their high margin – 50 percent or so – makes up for the slow inventory turn. In reality, it doesn’t. There are several accounting methods of illustrating the fallacy that high margins will yield high profits, even if inventory turns very slowly. The most-used measure is GMROI or Gross Margin Return on Investment. Without going into a long dissertation about GMROI and how it works, the bottom line is that jewelers should aim for faster inventory turn with smaller margins to maximize profits.

· Advertising Expense – Advertising costs, as a percentage of sales, are similar for both online and store-based merchants.

· Debt-to-Capital – Because of their heavy investment in inventory, store-based jewelers rely on high debt levels.

· Vendor Float – This is calculated by dividing “Accounts Payable” by “Inventory.” Retail jewelers typically pay their vendors on extended terms, so their vendor float is about four months. Because Blue Nile owns its inventory for just a few days, but pays for it in a few weeks, its vendor float is an astonishing 400 percent (if Blue Nile paid for the inventory as it sold it, the vendor float would be 100 percent; this calculation illustrates the power of negative working capital).

· Average Ticket – The typical mass market jeweler such as Kay or Zale generates an average ticket near $350. Higher-end guild jewelers generate an average ticket close to $1,200.

· Average Ticket DER (Diamond Engagement Ring) – Just under 70 percent of Blue Nile’s sales are diamond engagement rings, with an average ticket of about $5,900 in 2009 (this is down from a high of $6,200 in 2007, and reflects the recessionary environment). The typical independent specialty jeweler generates an average DER ticket of $4,500 or so, while chain jewelers generate an average DER ticket near $2,500. The demographic profile of the

· Sales Per FT (Full-Time) Employee – A sales associate in a typical specialty jewelry store can generate just under $250,000 in annual sales, based on the average of about 5 full-time equivalent employees in the typical independent jewelry store. At Blue Nile, the calculation of “sales per employee” includes all company employees;

· Sales Per Square Foot – The typical store-based jeweler utilizes a footprint of about 1,800 square feet (total including back room), and generates about $600 per square foot in annual sales. Blue Nile generates almost $5,000 in sales per square foot, including its corporate headquarters, its

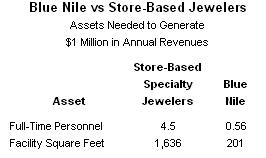

Assets Required to Generate $1 Million in Sales

There’s another way to compare the financial productivity of online jewelers such as

According to Jewelers of America, the typical specialty jeweler has about five full-time people and generates sales of $1.1 million. Further, the typical store size is 1,800 square feet. Online jeweler

Source: Blue Nile, Jewelers of America & Other |

Here’s what is important about this table:

· Personnel costs –

· Space costs – A store-based retail must spend heavily on a good retail location, so rent costs are high per square foot. On the other hand,

Because